Understanding State-Specific Estate Planning Laws

Planning for your estate can seem daunting, with many legal issues to navigate under Indiana state laws. Having an effective estate plan is important for your loved ones.

Understanding estate planning in Indiana will allow you to put your estate plans for your financial assets into place. It also spares your family the stress and uncertainty that comes with unclear directives.

This guide outlines statutes and procedures you need to know about state laws. Knowing Indiana’s state-specific estate planning laws will ensure that your affairs will be properly handled and that your legacy will be honored.

What Is The Probate Process?

Indiana’s probate process is a court-supervised procedure by which an estate plan is administered according to the deceased’s will. It can also implement an estate plan for decedents who pass without a separate will. Estate planning law dictates that most will go through probate, but state-specific laws determine which assets go through probate and which ones don’t.

This process stops scams and ensures that the decedent’s estate, including personal property, real property, and other assets according to property rights, end up in the right hands. As you’re making your estate plan, you’ll choose who will distribute your assets. This may be a family member or an estate planning lawyer.

State specific estate planning laws typically ze a person’s assets upon their passing to give the court time to evaluate if the will is state valid and acknowledge the executor. After that has occurred, your executor can move forward to resolve your estate matters.

Probate mandates that both financial institutions and beneficiaries must be notified after a will is accepted for probate.

What Happens to Your Assets in Probate?

Here’s what happens to your assets during estate administration:

Here’s what happens to your assets during estate administration:

- The deceased person’s assets are identified and cataloged by the executor/personal representative. This includes things like real estate, bank accounts, vehicles, personal property, investments, etc.

- The assets are appraised. Sometimes, professional appraisers are necessary.

- The remaining assets are temporarily frozen. The executor has legal control during probate, but beneficiaries cannot access inheritances, even with the power of an attorney.

- Once probate is completed, the executor distributes assets to beneficiaries according to the instructions in the will.

- Certain assets like life insurance, retirement accounts with named beneficiaries, and assets owned jointly often bypass probate and go directly to beneficiaries.

- Any contested matters around the will must be resolved before final distribution.

- The probate process provides court supervision, documentation, and validation of the settlement under the law.

Debts in Probate & Creditor Rights

Any financial debts are cleared up during probate. Debts, including property and inheritance taxes, are paid out of the funds that remain in the estate before distribution to the beneficiaries. According to Indiana state laws, creditor’s rights supersede the rights of the beneficiaries. Because of this, any prior debts must all be paid before any assets are distributed to beneficiaries.

Basically, the role of an executor is to perform the following:

- Account for all estate assets and their worth

- Ensure that the estate has paid any outstanding debts

- Provide for the orderly distribution of assets to beneficiaries

These must be done in order because it protects not only the creditors but also the beneficiaries. After all, no family members or other beneficiaries want to receive an inheritance only to find out that a creditor is pursuing those assets because he didn’t get paid!

To prevent that, the executor has a responsibility to make reasonable attempts to notify creditors so that they can pursue any legitimate claim.

Additional Laws, Regulations, and Legal Requirements

There are additional laws that govern unique circumstances, like the appropriate way to transfer ownership of assets.

These are complicated, which is why you have your estate plan reviewed by a knowledgeable estate planning attorney who can identify problems, solutions, and ensure that your financial affairs are in order before you pass away. The power of attorney could be key in this situation.

Even if you have knowledge about the laws governing Indiana including allowed probate avoidance methods, there may be other indirectly related laws that you don’t know to look out for.

Estate Planning for Small Estates

There aren’t laws for every situation. For example, Indiana state estate planning law makes it easier for smaller estates to be resolved quickly. Your estate can be settled using just an Affidavit whenever the total gross value of the estate is below $50,000.

There is also a 45-day waiting period from the time the decedent passes away. In determining the estate’s value, certain assets are excluded. These include assets with joint tenancy, accounts that are payable on death, property that transfers on death, and life insurance policies with named beneficiaries.

Indiana Estate Laws Passing on Wealth to Minor Children

It’s commonly asked how to pass wealth to minor children. Like many other jurisdictions, Indiana’s own laws do not allow minors to inherit any property directly. So, if you want to leave property to minors you must do it in a way that involves an adult managing it until the child reaches eighteen.

Trusts can help simplify this process since a Trustee will manage the child’s inheritance. There are other options as well, and you should discuss them with an attorney to determine which is right for you.

Laws Related to Marital Property

As opposed to being a community property state, Indiana follows the rules of equitable distribution for dividing marital assets acquired during the relationship. This means that when one spouse dies, the surviving spouse in Indiana is entitled to an equitable share of the marital assets accumulated during the marriage.

Unlike in community property states, any property that is considered to be held in what is known as “joint tenancy” automatically goes to the surviving tenant. Joint tenancy is a type of joint ownership most commonly seen when property is owned by married couples. Joint tenancy is also used by parents and their children or sometimes in instances where there are partners who are not related.

Unlike in community property states, any property that is considered to be held in what is known as “joint tenancy” automatically goes to the surviving tenant. Joint tenancy is a type of joint ownership most commonly seen when property is owned by married couples. Joint tenancy is also used by parents and their children or sometimes in instances where there are partners who are not related.

State laws seek to fairly divide marital property between the surviving spouse and any other beneficiaries named in the will. The distribution does not have to be exactly equal, but it should seek a reasonable balance based on respective ownership interests, financial contributions, and duration of the marriage.

Indiana recognizes tenancy by the entirety for property which passes wholly to the surviving spouse. Given Indiana’s equitable distribution approach, it’s advisable for spouses to clearly title their property and coordinate their estate plans to ensure their shared intentions for asset distribution are fulfilled.

Consulting an experienced estate planning attorney can help married couples in Indiana thoughtfully address property division issues and craft complementary wills and trusts.

State Specific Estate Planning Laws Inheriting a Life Insurance Policy

In most instances, determining who gets the benefits from a decedent’s life insurance policy has nothing to do with things like trusts or wills. That’s because life insurance policies are designed so that the policyholder names beneficiaries.

In Indiana, life insurance payouts go to named beneficiaries on the policy. Your insurance representative or attorney can help you file the state specific forms related to life insurance.

Federal Laws Regarding Probate

Indiana’s state specific estate planning laws are not the only ones that you need to be aware of. There are federal requirements regarding certain aspects of estate planning documents, and it is important to follow all federal and state laws.

- Federal Estate Taxes: Properties valued over the federal estate tax exemption are subject to federal estate and inheritance taxes. The executor is responsible for filing returns and paying any other estate taxes owed.

- Medicaid Estate Recovery: Medicaid may make a claim against the estate of a deceased recipient to recoup the costs of medical assistance paid. The claim is made during probate.

- Social Security: Social Security must be notified when a recipient dies so that payments may be discontinued.

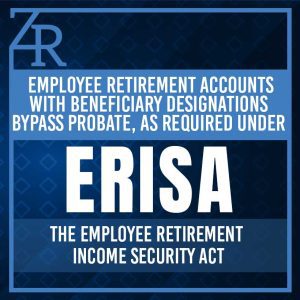

- ERISA: Employee retirement accounts with beneficiary designations bypass probate, as required under the Employee Retirement Income Security Act (ERISA).

- Veterans Benefits: The VA is notified upon a veteran’s death to discontinue benefits. Burial allowances and survivor benefits may need administration by the executor.

- Federal Crimes: If the deceased was convicted of a federal crime, probation or restitution orders may be addressed during probate.

- Tax Reporting: The executor handles any final income tax returns and tax filings.

Federal Estate Taxes: Properties valued over the federal estate tax exemption are subject to federal estate and inheritance taxes. The executor is responsible for filing returns and paying any other estate taxes owed.

Federal Estate Taxes: Properties valued over the federal estate tax exemption are subject to federal estate and inheritance taxes. The executor is responsible for filing returns and paying any other estate taxes owed.Estate Planning Tax Concerns

Any taxes owed must be paid after the decedent’s passing away. Several tax returns must be submitted, including a state income tax return and any one of three federal returns. Possible funding gains tax obligation issues and direct exposure to federal inheritance tax responsibility will require to be attended to.

Any taxes owed must be paid after the decedent’s passing away. Several tax returns must be submitted, including a state income tax return and any one of three federal returns. Possible funding gains tax obligation issues and direct exposure to federal inheritance tax responsibility will require to be attended to.

Knowledgeable Indiana tax advisors can answer questions about estate planning for taxes.

Indiana Estate Planning Laws Regarding Dying Without a Will

If someone passes away without a will, Indiana’s intestacy laws figure out where your properties go, based on intestate succession regulations.

Those regulations focus on successors starting with your closest family members like a spouse as well as kids, and then expand to consist of everybody from moms and dads and grandparents to relatives, nephews, nieces, etc.

FAQ:

Q: What is Probate?

A: Probate is the court and process that looks after people who cannot make their own personal, health care, or financial decisions. These people fall into three categories:

- Minors (under age 18 in most states)

- Incapacitated Adults

- People who have died without a will or other form of legal arrangement

The individuals who make an estate plan to avoid probate court accomplish three specific goals:

- Save money

- Avoid the legal wrangling of probate court

- Prevent personal affairs from entering into the public record

The individual circumstances surrounding the death of a specific person and their end-of-life planning will determine how long the probate period will last.

Q: What is a Will?

A: The will is one of the estate planning documents that an individual creates so that they can ensure the orderly disposition of all of their assets after they pass. Wills don’t avoid the probate process as wills have no legal authority until the creator dies and the original will is then delivered to the Probate Court.

Q: What is a Living Will?

A:  Living Wills are commonly called Advance Medical Directives, and they determine who can make decisions regarding your medical care. The purpose of a living will is so an individual can state their wishes in the instance that that individual may potentially be placed on life support. Health care directives like these are executed with a Durable Power of Attorney in the following situations:

Living Wills are commonly called Advance Medical Directives, and they determine who can make decisions regarding your medical care. The purpose of a living will is so an individual can state their wishes in the instance that that individual may potentially be placed on life support. Health care directives like these are executed with a Durable Power of Attorney in the following situations:

- An individual may be placed on life support

- An individual is incapacitated and in a terminal condition

The Durable Power of Attorney allows an individual the legal ability to make decisions regarding medical decisions if an individual is incapacitated. Power of Attorney ends when a person dies and there are no longer any decisions to be made regarding medical information or medical treatment.

Q: What is a Revocable Living Trust?

A: These legal documents can change over time. They’re used to avoid probate and protect the privacy of the trust owner and beneficiaries of the trust and to minimize other taxes.

Q: What is an Irrevocable Living Trust?

A: This trust cannot be revoked or changed. They’re almost exclusively created for the benefit of producing a very specific set of tax or form of asset protection. Both kinds of living trusts come with estate planning documents important to your directives.

Protect Your Legacy with Zentz & Roberts

At Zentz & Roberts, P.C we’ll create an estate plan within your state lines that follow the Indiana Estate Law and file your estate planning documents. We’re even up to date on new state’s laws. When you’re ready to create an estate plan, contact the Indiana estate planning law firm, Zentz & Roberts, P.C, at 317-220-6056 to schedule an estate plan.

***Please note: This page is not intended to give specific legal advice but is meant for information purposes only. Contact us to discuss your case***